How climate risk and rising premiums are redefining post-grad life

Last week, the paths of Wheaton College disappeared beneath nearly 32 inches of snow as Winter Storm Hernando paralyzed Eastern Massachusetts, resulting in cancelled classes and extended deadlines. But beyond campus inconvenience, the storm entered another system entirely: insurers’ risk models.

Globally, climate shocks are widening what insurers call the protection gap. In 2025 alone, disasters caused roughly US$224 billion in losses, yet less than half were insured, shifting over $100 billion in costs onto governments, taxpayers, and households.

In California, after successive wildfires produced tens of billions in insured losses, major insurers such as State Farm, Allstate, and Farmers began cancelling policies, refusing renewals, or withdrawing from high-risk regions altogether. Homeowners suddenly found coverage unavailable or unaffordable, forcing thousands onto the state’s insurer-of-last-resort plans.

While Norton does not face wildfires, a report from Mass.gov notes that increased flooding and severe weather along the Massachusetts coastline, driven by climate change, are already affecting insurance markets. Enrollment in the Massachusetts FAIR Plan—the state’s backup insurer for properties private companies will not cover—has increased in recent years, particularly on the Cape and Islands, where nearly two out of five homeowners now rely on last-resort coverage.

Moreover, FAIR Plan policies often exclude liability or water damage coverage. This bare-bones plan is then combined with a concentration of risk: as private insurers cherry-pick safe zip codes using increasingly sophisticated pricing mechanisms that leverage satellite imagery—roof conditions, vegetation density, or proximity to hazard zones—AI models, and property-level indexing, the FAIR Plan is left with high-risk properties. According to Insurance Business, the California FAIR Plan has proposed an average home insurance rate increase of 35.8%, the largest in seven years.

What’s Causing This?

As climate change increases the frequency and unpredictability of disasters, undermining the historical data insurers rely on to price risk, the technology used to price risk is becoming increasingly precise and predictive. (The ethics of using automated property-level indexing systems and satellite imagery is another conversation altogether.) Plus, rebuilding has become dramatically more expensive as inflation, labor shortages raise the cost of every claim.

Moreover, global reinsurance markets—the insurers of insurers—have tightened their belts as well as their coverage terms after years of massive catastrophe losses worldwide, passing higher costs even to regions that avoided direct hits.

In 2024, global insured losses reached approximately $140 billion, continuing a long-term upward trend of 5–7% annual growth. While “peak” disasters like Hurricanes Helene and Milton dominated headlines, the real driver of rising losses is quieter: the relentless accumulation of “non-peak” perils—like wildfires, floods, and severe convective storms—which now consistently generate nearly $100 billion in annual losses. In 2025 alone, these “secondary” hazards caused $98 billion in insured losses, nearly triple the 30-year inflation-adjusted average of $33 billion.

Reinsurance capital is a global pool. Consequently, rising catastrophe losses everywhere, from Florida and California to Central America and Southeast Asia, spiked costs for regional U.S. insurers, including those in Massachusetts, that buy “reinsurance” from the same global giants like Swiss Re and Munich Re. Those costs trickled down as home insurance premiums rose 8.5% in 2025 and are projected to rise another 8% in 2026, a 17.2% compounded increase in two years — a financial shock that far outpaces wage growth — turning climate risk into a recurring household expense.

How Does this Affect You, a Student?

Insurance costs often arrive indirectly, through higher rent as landlords pass rising property insurance premiums on to tenants, mandatory renter’s insurance policies built into leases, and car insurance rates affected by increasingly volatile weather patterns. Moreover, if you dream of buying a home, while low-risk neighborhoods are becoming too expensive to enter, in high-risk neighborhoods, it is effectively impossible to secure a mortgage unless you can first secure—and afford—the insurance. Insurers are increasingly using predictive “frequency-severity” climate modeling rather than just looking at past driving records. If data shows that Norton, MA, is experiencing more frequent “flash freeze” events, the entire town gets re-rated.

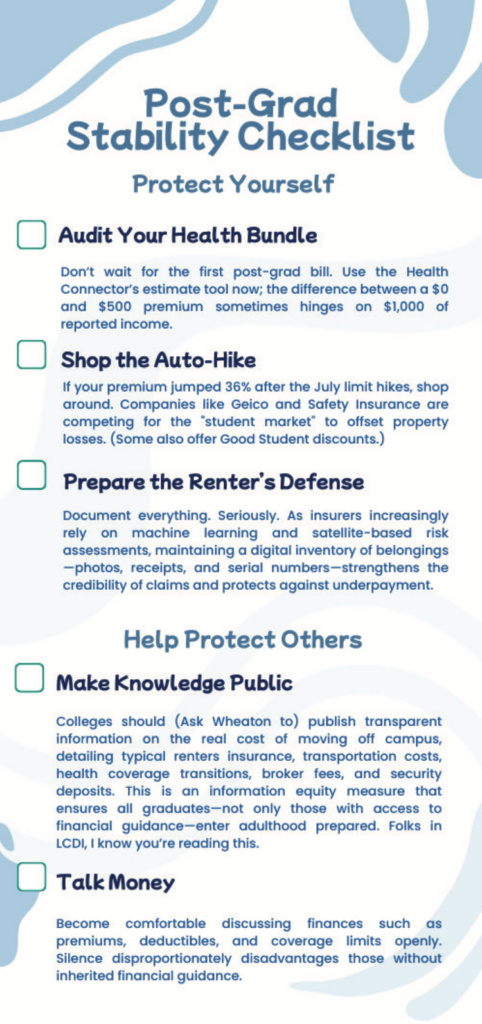

Effective July 2025, Massachusetts raised mandatory auto insurance minimums, jumping Property Damage Liability from $5,000 to $30,000 to reflect modern repair realities. A 2020 fender bender that cost $2,000 now exceeds $7,000 due to embedded sensors and LIDAR technology.

For the average 22-year old graduate, this burden manifests as a “commuter tax.” As premiums remain heavily age-weighted, a young driver often pays 2.5 times as much as a 40-year old for the exact same vehicle. This financial hurdle is compounded by a brutal housing market; as affordability crises push the Class of 2026 further from urban employment centers, car ownership is no longer a luxury—it is a compulsory, rising expense. For the Wheaton senior planning a post-grad life in Boston, the road ahead just became significantly more expensive.

And, oh, wait, there’s still health insurance.

Across the United States, rising medical costs, demographic change, and uncertain federal funding structures have driven premium increases that ripple far beyond individual households. In Massachusetts, the Health Connector, which allows young adults between jobs, fellowships, and graduate programs to maintain affordable coverage, was the “post-graduation bridge” for Wheaton seniors transitioning into the workforce for years. Now, with the expiration of federal Enhanced Premium Tax Credits (ePTCs) in December 2025, this bridge is hanging by a thread. While Governor Healey committed $250 million to shield the lowest-income households, those earning modest professional salaries (around US$65,000) are now exposed. For a new graduate in Boston, benchmark premiums can now exceed $500 per month.

This transition is particularly jarring as, before graduation, colleges negotiate group coverage (the Student Health Insurance Plan (SHIP)), pool risk across thousands of students, and buffer students from the volatility of the larger insurance market. Graduation abruptly sinks that SHIP.

Furthermore, where previous generations chose cities based on opportunity or preference, young adults increasingly face a different question: Where can I afford to live stably? Some graduates retain mobility because family wealth absorbs these shocks. Others find their futures constrained not by ambition, but insurability.

Welcome to climate gentrification. As climate risk reshapes housing markets, safer, higher-resilience neighborhoods become increasingly valuable. In cities from Miami to New Orleans, areas less exposed to flooding or disaster are attracting investment and higher-income residents, driving up property values and quietly displacing long-standing communities. Flood-exposed coasts, wildfire-prone California, and the hurricane corridor across Florida and the Gulf are already losing decent, affordable coverage.

This is no longer just a climate—or even financial—story. It is a sociology story, and it is global. Across the Global South, low-emitting regions—from drought-stricken Central America driving migration northward, to flood-vulnerable Bangladesh and Pakistan, typhoon-exposed Philippines, and hurricane-hit Caribbean nations facing insurance retreat— bear the harshest climate displacement pressures. Yet as migration pressures rise, much of the Global North, accountable for high historical emissions, responds with fortified borders, externalized asylum systems, and expanding surveillance— from deadly Mediterranean crossings to U.S. asylum backlogs and offshore migration controls in Europe and Australia.

Climate change, alongside the quiet evaporation of financial safety nets like insurance, is reorganizing the global hierarchy of security and mobility—deciding who moves freely and whose movement is criminalized, sorting lives by wealth, nationality, race, gender and even age.